The Affordable Care Act (ACA) went into effect over a decade ago on January 1, 2014. While we would hope that it is second nature by now, we find that for many, the year-end deadline still sneaks up on us and causes undue stress. Confucius said “Success depends upon previous preparation, and without such preparation, there is sure to be failure,” so with a little bit of preparation now, one can be ahead of the game when we get to December. Here is what can be done ahead of time: It goes, without saying, that the first step is determining…

Posts published in “Affordable Care Act (ACA)”

Selecting a health insurance plan for your employees is harder than ever, with the exponentially rising costs and endless number of plans. Not only are there many different carriers to choose from, but there are also three different types of plans available: Fully-insured health plan: You may even call this the traditional insurance plan, where the employer pays a monthly premium and the insurance company pays all claims. Self-funded health plan: This is where the insurance company is paid an administrative fee and the employer acts as the insurer, paying the claims as they are incurred. This plan is typically…

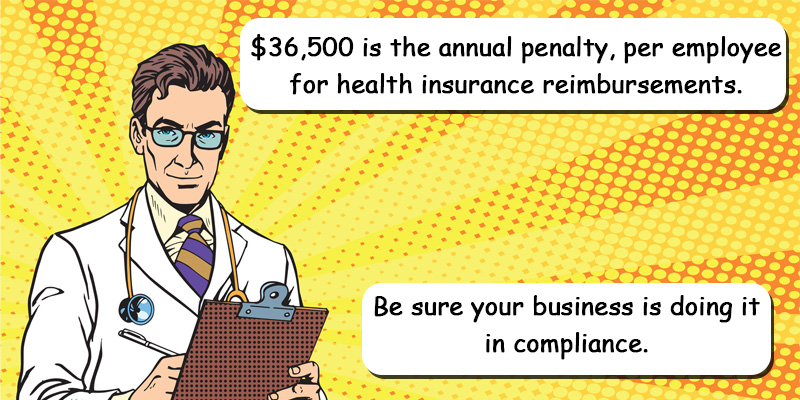

As we get into the health insurance renewal season, there are some smaller, non-ACA mandated businesses (less than 50 FTEs) that may consider dropping their small group health plan all together. An average of 20-30% group rate hikes year after year do take a toll on the bottom line, so it would not be surprising. In lieu of carrying a group health plan, some employers may even decide to simply reimburse their employees a set amount for them to obtain individual coverage, or maybe even pay for the employees individual health insurance costs directly. Unfortunately, 2013 guidance from the IRS…

Yesterday, November 18, the IRS issued Notice 2016-70, which extends the due date for the 2016 requirement to furnish ACA-related statements to individuals for insurers, self-insuring employers, and certain other providers of minimum essential coverage under I.R.C. § 6055, and for applicable large employers under I.R.C. § 6056, and extends good-faith transition relief from section 6721 and 6722 penalties to the 2016 information-reporting requirements under sections 6055 and 6056. The due date is extended from January 31st, 2017 to March 2nd, 2017. The notice also provides guidance to individuals who, as a result of these extensions, might not receive a…

Today, December 28th, 2015, the Internal Revenue Service issued Notice 2016-4, which extends the due dates for 2015 Information Reporting under I.R.C. sec 6055 and 6056, which includes the 1095-B and C forms and the 1095-B and C forms. This is great news for the many employers faced with the new filing requirements of these forms, and provides them with additional time to get their information together. The extended due date to issue the 1095-B or 1095-C forms to full-time employees has been extended from February 1st, 2016 to March 31st, 2016, as well as an extension of filing the forms to the…

I have a client with a very interesting scenario in regards to Affordable Care Act (ACA) compliance and their desire to abide by the law. This client is defined as an Applicable Large Employer (ALE) by having greater than 50 Full-time Equivalent employees, therefore is bound by the Employer Shared Responsibility provisions under 4980H of the Internal Revenue Code. If they do not offer affordable health coverage to their full-time employees, they may be subject to a penalty of $2,000 per employee. In this case, the company, not wanting to be penalized, sought a health insurance agent to obtain a…

This past week, the Internal Revenue Service has published the final versions of Forms 1094-C and 1095-C, and their respective instructions for tax year 2015. These forms will be used by employers to report offers of health insurance coverage made to their full-time employees after year end. While not much has changed on the forms themselves from the earlier draft, there has been some clarification in reporting in the final version of the instructions. Applicable large employers (ALE) must file these forms with the IRS annually, no later than February 28 (March 31 if filed electronically) of the year immediately…